Galaxy FCT - Solid H2 Logistics

Solid H2 Logistics

Introducing the Fundamentals

Conceptually, Solid H2 Logistics bypasses the need to fight the physics of H2 Gas at every segment of the supply chain. H2 is "packaged into Sodium Borohydride (NaBH4) at the point of production. All logistics is carried out in its solid form and H2 Gas is released only "on demand" at user location via a hydrolysis reaction (no external energy input required). This provides safe, simple and cost effective logistics throughout the entire supply chain

Sodium Borohydride (NaBH4) is energy dense, non-flammable and can be stored at ambient temperature without pressure. We can release 120 kg of H2 Gas from 1 m3 compared to 71 kg of H2 Gas from Liquid H2. As further comparison, high pressure compressed gas at 700 bar delivers about 42 kg of H2 per m3.

NaBH4 has been around Since the 50s … Why NOW?

It was "a bridge too far" …

For a long time, there were essentially two main bottlenecks that made the use of Solid H2 (NaBH4) for clean energy logistics, clearly "a bridge too far". First, NaBH4 cost too much. Secondly, the ability to release H2 gas rapidly and efficiently from solid form NaBH4 is a recent breakthrough by Galaxy FCT. In the past, when the liquid form of NaBH4 was used, it suffered from poor "weight/volume to power" ratio and there were also issues with reaction efficiency.

For More information on Galaxy FCT and our

Technology Breakthrough, please see

"Introduction to Galaxy FCT"

We do not believe that the price of NaBH4 should be where it is today …

NaBH4 prices today is way too high to be considered seriously as a mainstream vector for clean energy logistics. But this should not be the case in the future. Let's take a deeper dive. To start with, NaBH4 is sold today as a specialty chemical . Global production volumes are relatively small (just above 100,000 tons per year) and production is typically carried out in batches in mature integrated chemical facilities … using mostly the Brown Schlesinger process which was developed in 1953.

The "Tipping Point" is here.

Apart from the breakthrough that Galaxy FCT has made, the urgency to avert Climate Disaster has brought incredible progress in our ability to generate energy from renewable sources (especially Solar and Wind). This, together with the impressive progress made in the associated supply chains (batteries, electrolyzers and fuel cells) has contributed substantially to our ability to take on the challenge of bringing down the production costs of NaBH4. The tipping point is close … and the time for a paradigm shift is here.

The Conceptual "TRADE-OFF" Underpinning Solid H2 Logistics

Its easier to deal with "Production Costs" than to fight the physics of H2 across the entire supply chain …

Conceptually, Solid H2 Logistics is a strategic "trade-off". Put very simply, we get efficient storage and logistics in return for accepting high "production/packaging" costs (for simplicity, I will just call them "Production Costs").

"BEYOND PARETO" …

Solving "Production Costs" is now the 10% that could bring you 90% of the results … We need to address it with an unrelenting focus because this is where the battle will be won.

Hydrogen has been anointed as the "green energy molecule" of choice to complement the electricity grid in our desperate battle to stave off Climate Disaster. This will inevitably make the H2 supply chain of the immediate future incredibly long (stretched way out of its comfort zone) and complex, requiring storage at various stages of the supply chain to deal with the vagaries and mismatches between intermittent producers and every type of user that you can imagine. If fighting the physics of H2 Gas is tough, its going to get a whole lot tougher.

"PRIME SITE" Renewables Dedicated to NaBH4 Production

Let's produce at massively unprecedented scale where energy is (or will be) "dirt cheap" in the not so distant future …

Given the urgency of global decarbonization, there is every reason to "go big" or to "go home". Our thirst for green energy molecules which can be easily stored, moved and distributed (just like hydrocarbons, but only easier) has never been greater. Recognizing that the biggest cost component in NaBH4 production is in fact energy, developing massive renewable farms dedicated to NaBH4 production at the highest yielding locations on the planet (lets call them "Prime Sites") and dispensing with the need for transmission infrastructure would be the perfect way to start.

"PRIME SITE" production will

be a game changer …

Integrated Prime Site NaBH4 production will also bring about the following advantages:

- Much higher productivity per unit Capex (e.g. per Solar PV Panel);

- Abundance of Unused Land at Low (or no) Cost;

- No Need for Transmission or Off-take Arrangements;

- "Shovel Ready" for Immediate Execution.

A continued unrelenting focus will ensure that production costs keep coming down over time in tandem with the incredible way Solar PV and Wind Turbines prices are moving.

This first "Giant Step" will bring NaBH4 prices substantially lower from where they are today. Clearly, such a plant would be configured very differently from existing plants today (built mainly 20 -30 years ago) as it will take advantage of the latest process technology and optimizations that such unprecedented scale will allow, including backward integration into all raw/intermediate material to ensure lowest cost production.

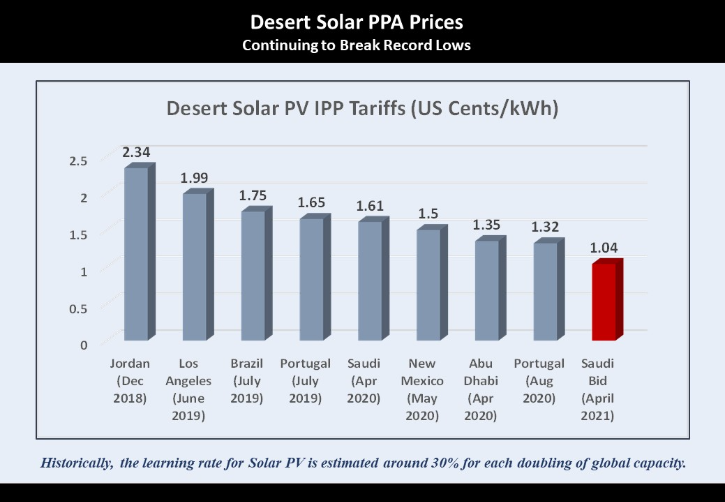

Wrights Law at Work - Solar PV

Solar PV - Clearest illustration of Wrights Law at Work.

In 1936, William Theodore Wright postulated that the "Cost of a unit of manufacturing will decrease proportionally as a function of cumulative production". The way this has been working with Desert Solar is nothing short of incredible. In April 2021, the latest bids for Dessert Solar on a 600 MW project in Saudi Arabia hit a new record low of 1.04 Cents (US) per kWh, a whopping 20% lower than the last record set in Portugal just 8 months ago.

A kWh of electricity in the Desert costs a whole lot less from a kWh of electricity delivered in New York City …

In monetary terms, it will not be long before the "Energy Penalty" will be eventually be "CRUSHED"

Historical data suggests that the learning rate for solar has been around 30% for each doubling of capacity. With current market share of only about 7% of global energy requirements, there is much more room to run. Given energy is the single largest cost factor, the production costs of NaBh4 should follow in the same trajectory.

It has happened in the past with Semiconductors, Solar PVs, Wind Turbines and Lithium Batteries … there is no reason to believe why it will not happen with NaBH4.

It is pertinent to note that there are no particularly "supply constrained" critical minerals or particularly expensive ingredients required in meaningfully large quantities for the production of NaBH4. The principal inputs are Sodium (from NaCl), Hydrogen (from H2O), and Boron. Energy is the largest single production cost factor (to produce Sodium and H2). As such, if we are looking at NaBH4 to stand at the heart of clean energy logistics, every factor points towards production of NaBH4 from the lowest cost renewable energy, generated at unprecedented scale in the most productive locations on planet earth.

Future Cost Reduction Road Map for NaBH4

Cost reduction is expected to Continue …

We believe that the future price of NaBH4 will continue to move down similar to what we have witnessed in Solar PV, Wind Turbines and Lithium Batteries in recent years. The key drivers that we can foresee are summarized below.

As more "Prime Site" production sites are carried out, the massive scale will further accelerate the learning rate of all associated renewables, resulting in lower costs all round and this cycle will be expected to continue over time to bring production costs of NaBH4 even lower.